|

The Week Ahead: Highlights

Asia-Pacific Preview

Asia Data Expected to Show More Iran War Effects

By Brian Jackson, Econoday Economist

The main focus of Asia-Pacific data will be the monthly

PMI surveys from S&P for the region. Last month's surveys

generally showed the Iran conflict continued to impact activity and sentiment,

with respondents across the region reporting higher costs and supply delays.

Some also cautioned that increased production partly reflected

precautionary stockpiling motivated by concerns about potential further

disruptions and cost increases. June surveys may show some moderation in these

concerns following progress in improving access through the Straits of Hormuz.

China's official PMI surveys will also be published in

addition to the S&P surveys. The official surveys showed very subdued

conditions in both the manufacturing and non-manufacturing sectors in May, with

subsequent activity data showing weaker growth in retail sales and investment.

South Korea reports industrial production, retail sales,

trade, and inflation data next week, with these releases set to shape

expectations for the next Bank of Korea meeting later in the month. South

Korea's growth has been supported by exports of AI-related technology while

headline inflation rose to its highest level since 2024 in May.

US Preview

Jobs Report Up Next

By Theresa Sheehan, Econoday Economist

The June 29 week sees the lead up to the Independence Day

observance on Saturday, July 4 with a federal holiday on Friday. With a

three-day weekend on the horizon, many workers will take vacation time to fill

out the week. Retailers online and brick-and-mortar will be offering

discounts and incentives to get customers into stores. Given the price of

gasoline and other rising costs associated with travel, people may be staying

nearer home for their vacation activities. Staycationers may be visiting home and

garden centers to take on home projects and for outdoor entertainment items.

Those who are traveling may contribute to higher spending on things like

restaurants and lodging.

For the week's economic data, the Friday holiday means that

the timing of some reports will be moved up, most notably the monthly

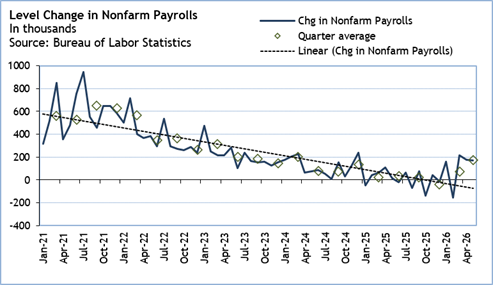

employment report for June to 8:30 ET on Thursday. The June report could well

see hiring in similar industries as took place in May, but probably to a lesser

extent. May saw jobs added in leisure and hospitality and local government that

were likely associated with preparations for the July 4th

celebrations related to the 250th anniversary of the Declaration of

Independence. There may be some additional hiring for those sorts of functions

in June. However, many of these jobs will go away after the July survey

reference period.

The ongoing demand for workers in healthcare should continue

but this appears to be trending downward. Other service-providing industries

are simply not hiring, although most are also not laying off workers at least

not yet. Gains among goods-producers are modest and probably due to increased

supply of skilled labor that these industries have needed for some time. The

overall change in payrolls has been a bit stronger so far in 2026 but

uncertainty about the economy remains elevated.

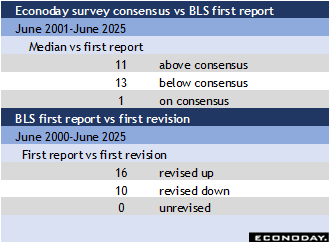

The June payroll numbers are about as likely to come in

above consensus as below, but are also slightly more likely to be subsequently

revised higher.

The Week Ahead: Econoday Consensus Forecasts

Monday

Japan Retail Sales for May

Consensus Forecast, M/M: 0.6%

Consensus Range, Y/Y: -2.3% to 1.0%

Consensus Forecast, Y/Y: 3.5%

Consensus Range, Y/Y: 1.0% to 4.3%

Japanese retail sales are seen rising for a third straight

month on the year in May, supported by solid growth in department store sales

and a smaller decline in fuel prices than in the previous month, providing

momentum for overall retail sales.

May retail sales are expected to rise 3.5 percent, matching the strongest

increase since April 2025, when they climbed by that amount. This compares with

a revised 2.8 percent increase in April, which was sharply revised up from the

preliminary reading of 2.1 percent.

Retail sales in April were supported by continued demand for clothing and

luxury goods at department stores, a recent pickup in vehicle purchases, and

robust sales of drugs and cosmetics, offsetting the impact of lower fuel prices

resulting from subsidies aimed at easing the burden of the Middle East

conflict.

On a month-on-month basis, sales are projected to rise 0.6 percent, following a

revised 2.1 percent gain in April, up from the preliminary reading of a 1.3

percent increase.

India Industrial Production for May (Mon 1600 IST; Mon

1030 GMT; Sun 0630 EDT)

Consensus Forecast, Y/Y: 4.5%

Consensus Range, Y/Y: 3.6% to 5.2%

Industrial output expansion expected to slow to 4.5 percent

in May from 4.9 percent in April, showing weaker growth due to the effect of

the Mideast war.

Eurozone M3 Money Supply for May (Mon 1000 CEST; Mon

0800 GMT; Mon 0400 EDT)

Consensus Forecast, Y/Y-3-Month Moving Average: 2.7%

Consensus Range, Y/Y-3-Month Moving Average: 2.6% to 2.9%

The consensus sees money growth slowing to 2.7 percent in

May from 2.9 percent in April.

Eurozone EC Economic Sentiment for June (Mon 1100

CEST; Mon 0900 GMT; Mon 0500 EDT)

Consensus Forecast, Economic Sentiment: 94.1

Consensus Range, Economic Sentiment: 91.5 to 94.5

Consensus Forecast, Industry Sentiment: -8.1

Consensus Range, Industry Sentiment: -9.0 to -8.0

Consensus Forecast, Consumer Sentiment:

Consensus Range, Consumer Sentiment: to

Economic sentiment seen somewhat better at 94.1 in June from

93.5 in May in response to lower energy costs and apparent progress toward a

settlement in the US-Iran war. Sentiment remains depressed relative to January.

Tuesday

South Korea Industrial Production for May (Tue 0800

KST; Mon 2300 GMT; Mon 1900 EDT)

Consensus Forecast, M/M: 0.5%

Consensus Range, M/M: 0.4% to 1.7%

Consensus Forecast, Y/Y: 3.1%

Consensus Range, Y/Y: 2.1% to 4.3%

The consensus looks for industrial output to rebound by 0.5

percent on the month in May and 3.1 percent on year after falling 0.6 percent

on the month and rising a modest 1.5 percent on year in April.

Japan Unemployment Rate for May (Tue 0830 JST; Mon

2330 GMT; Mon 1930 EDT)

Consensus Forecast, Rate: 2.6%

Consensus Range, Rate: 2.5% to 2.6%

Persistent labor shortages in Japan are expected to keep the

unemployment rate near a nine-month low in May, with the seasonally adjusted

jobless rate forecast to edge up to 2.6 percent from April's 2.5 percent, the

lowest level since July 2025. The jobless rate fell to a nine-month low in

April as many workers changed jobs at the start of the new fiscal year.

Japan Industrial Production for May (Tue 0850 JST;

Mon 2350 GMT; Mon 1950 EDT)

Consensus Forecast, M/M: 1.3%

Consensus Range, M/M: 0.8% to 2.3%

Consensus Forecast, Y/Y: -0.9%

Consensus Range, Y/Y: -1.4% to 0.1%

Japanese industrial output is expected to rise for a second

straight month in May after posting an unexpected increase in the previous

month, even as the geopolitical tensions in the Middle East stayed in place.

Solid domestic business sentiment and continued growth in exports are seen

supporting production on a month-on-month basis, although output is expected to

fall from a year earlier for the first time in six months.

Industrial production in May is projected to rise 1.3

percent on the month, following a revised 0.5 percent increase in April. The

forecast is broadly in line with the Ministry of Economy, Trade and Industry's

adjusted production forecast index, which points to a 2.1% increase in output

during the month.

On a year-on-year basis, output is expected to fall 0.9

percent in May, marking the first decline in six months, after a revised 2.0

percent increase in April from the initial 2.3 percent.

China CFLP Composite PMI for June (Tue 0930 CST; Tue

0130 GMT; Mon 2130 EDT)

Consensus Forecast, Composite Index: 49.9

Consensus Range, Composite Index: 49.6 to 50.5

Consensus Forecast, Manufacturing Index: 50.1

Consensus Range, Manufacturing Index: 49.8 to 50.3

Consensus Forecast, Non-Manufacturing Index: 49.9

Consensus Range, Non-Manufacturing Index: 49.9 to

50.7

Economic activity expected to continue hovering around the

breakeven 50 index reading in June, indicating no growth and no contraction.

The composite index is expected at 49.9, down from 50.1 in May. Manufacturing

seen at 50.1 in June versus 50.0 in May and non-manufacturing expected down at

49.9 versus 50.5 in May.

Germany Retail Sales for May (Tue 0800 CEST; Tue 0600

GMT; Tue 0200 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: 0.0% to 0.4%

Sales expected up a marginal 0.1 percent in May after

declining 0.3 percent in April.

UK GDP for First Quarter (Tue 0700 BST; Tue 0600 GMT;

Tue 0200 EDT)

Consensus Forecast, Q/Q: 0.6%

Consensus Range, Q/Q: 0.6% to 0.6%

Consensus Forecast, Y/Y: 1.1%

Consensus Range, Y/Y: 1.1% to 1.1%

The final revision for Q1 is expected to show no change from

the 0.6 percent Q/Q figure but the year/year is seen at 1.1 percent versus 1.2

percent reported previously.

France CPI for June (Tue 0845 CEST; Tue 0645 GMT; Tue

0245 EDT)

Consensus Forecast, M/M: 0.0%

Consensus Range, M/M: 0.0% to 0.4%

Consensus Forecast, Y/Y: 2.3%

Consensus Range, Y/Y: 2.1% to 2.4%

CPI seen flat on the month and up 2.3 percent on year in

June after 0.1 percent and 2.4 percent in May.

Germany Unemployment Rate for June (Tue 0955 CEST;

Tue 0755 GMT; Tue 0355 EDT)

Consensus Forecast, Rate: 6.4%

Consensus Range, Rate: 6.3% to 6.4%

The jobless rate is expected to tick up to 6.4 percent in

June from 6.3 percent in May.

Italy CPI for June (Tue 1100 CEST; Tue 0900

GMT; Tue 0500 EDT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.2% to 0.4%

Consensus Forecast, Y/Y: 3.3%

Consensus Range, Y/Y: 3.2% to 3.4%

CPI seen at 0.4 percent and 3.3 percent in June versus 0.4

percent and 3.2 percent in May.

Germany CPI for June (Tue 0800 CEST; Tue 0600 GMT;

Tue 0200 EDT)

Consensus Forecast, M/M: 0.1%

Consensus Range, M/M: -0.1% to 0.3%

Consensus Forecast, Y/Y: 2.7%

Consensus Range, Y/Y: 2.5% to 2.9%

Consensus Forecast, HICP - M/M: 0.1%

Consensus Range, HICP - M/M: -0.1% to 0.4%

Consensus Forecast, HICP - Y/Y: 2.8%

Consensus Range, HICP - Y/Y: 2.5% to 3.0%

CPI expected up 0.1 percent on month and 2.7 percent on year

in June after minus 0.2 percent and up 2.6 percent in May.

Canada Monthly GDP for April (Tue 0830 EDT; Tue 1230

GMT)

Consensus Forecast, M/M: 0.4%

Consensus Range, M/M: 0.3% to 0.4%

Forecasters agree, as usual, with the Statistics Canada

preliminary estimate, showing 0.4 percent growth on the month in April as Q2

gets off to a better start after no change in Q1.

US Case-Shiller 20-City Home Price Index for April (Tue

0900 EDT; Tue 1300 GMT)

Consensus Forecast, 20-City Adjusted - M/M: -0.1%

Consensus Range, 20-City Adjusted - M/M: -0.2% to

0.1%

Consensus Forecast, 20-City Unadjusted - Y/Y: 1.0%

Consensus Range, 20-City Unadjusted - Y/Y: 0.8% to 1.6%

Case-Shiller seen down 0.1 percent on the month, seasonally

adjusted, and up 1.0 percent on year for April. That is not far off the March performance

when prices declined 0.2 percent on the month and rose 1.0 percent on year.

US FHFA House Price Index for April (Tue 0900 EDT;

Tue 1300 GMT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: 0.1% to 0.2%

Consensus Forecast, Y/Y: 2.1%

Consensus Range, Y/Y: 2.1% to 2.1%

Rather more buoyant than the forecast for Case-Shiller index,

the consensus sees house prices up 0.2 percent on the month in April and up 2.1

percent on year.

US Chicago PMI for June (Tue 0945 EDT; Tue 1345 GMT)

Consensus Forecast, Index: 55.2

Consensus Range, Index: 51.0 to 61.3

Forecasters expect another upbeat report with the Chicago

PMI at 55.2 in June versus 62.7 in May. That would suggest ongoing good expansion

in business activity in the region after years of contraction.

US Consumer Confidence for June (Tue 1000 EDT; Tue

1400 GMT)

Consensus Forecast, Index: 94.5

Consensus Range, Index: 92.5 to 97.5

Consumers are feeling a bit better now that gas prices are

off their peak. The consensus looks for the index at 94.5 in June, up from 93.1

in May and 93.8 in April in the Conference Board report. The separate

University of Michigan consumer sentiment survey already showed sentiment up 10

percent in June from May.

US JOLTS for May (Tue 1000 EDT; Tue 1400 GMT)

Consensus Forecast, Job Openings: 7.307 M

Consensus Range, Job Openings: 6.975 M to 7.600 M

The consensus sees job openings down at 7.307 million unit

rate in May from 7.618 million in April. That would suggest lower demand for

workers consistent with a low-hire, low-fire economy.

Wednesday

Japan Tankan for Second Quarter (Wed 0850 JST; Tue

2350 GMT; Tue 1950 EDT)

Consensus Forecast, Large Manufacturer Sentiment Index:

15

Consensus Range, Large Manufacturer Sentiment

Index: 14 to 18

Consensus Forecast, Large Non-Manufacturer Sentiment

Index: 36

Consensus Range, Large Non-Manufacturer Sentiment Index:

34 to 37

Consensus Forecast, Small Manufacturer Sentiment Index:

4

Consensus Range, Small Manufacturer Sentiment

Index: -3 to 6

Consensus Forecast, Small Non-Manufacturer Sentiment

Index: 14

Consensus Range, Small Non-Manufacturer Sentiment Index:

-2 to 17

FY Current, 2025

Consensus Forecast, Large Firms Capital Expenditure

Plans: 10.2%

Consensus Range, Large Firms Capital Expenditure Plans:

9.0% to 12.0%

Consensus Forecast, Small Firms Capital Expenditure

Plans: -4.2%

Consensus Range, Small Firms Capital Expenditure Plans:

-4.6% to -2.4%

South Korea External Trade for June (Wed 0900 KST; Wed

0000 GMT; Tue 2000 EDT)

Consensus Forecast, Balance: $33.1 B

Consensus Range, Balance: $29.9 B to $34.4 B

The surplus is expected to widen to $33.1 billion from $27.0

billion in May as exports remain buoyant on the AI data center buildout using

Korean chips.

China PMI Manufacturing for June (Wed 0945 CST; Wed

0145 GMT; Tue 2145 EDT)

Consensus Forecast, Index: 51.9

Consensus Range, Index: 51.4 to 52.0

The manufacturing PMI is seen almost unchanged at 51.9

versus 51.8 in May, indicating very slow expansion in business activity, a

better reading than the official Chinese PMI which is expected to show no

growth and no contraction.

France PMI Manufacturing Final for June (Wed 0850

CEST; Wed 0650 GMT; Wed 0250 EDT)

Consensus Forecast, Index: 50.7

Consensus Range, Index: 50.7 to 50.7

The consensus looks for no revision in the June final from

the June flash at 50.7, but up from 49.7 in May.

Germany PMI Manufacturing Final for June (Wed 0955

CEST; Wed 0755 GMT; Wed 0355 EDT)

Consensus Forecast, Index: 50.0

Consensus Range, Index: 50.0 to 50.1

The consensus calls for no revision in the June final from

the June flash at 50.0 versus 50.1 in May.

Eurozone PMI Manufacturing Final for June (Wed 1000

CEST; Wed 0800 GMT; Wed 0400 EDT)

Consensus Forecast, Index: 51.3

Consensus Range, Index: 48.9 to 51.6

The consensus looks for no revision in the June final from

the June flash at 51.3, versus 51.6 in May.

UK PMI Manufacturing Final for June (Wed 0930 BST; Wed

0830 GMT; Wed 0430 EDT)

Consensus Forecast, Index: 53.1

Consensus Range, Index: 49.4 to 53.1

The consensus looks for no revision in the June final from

the June flash at 53.1 versus 53.9 in May.

Eurozone HICP Flash for June (Wed 1100 CEST; Wed 0900

GMT; Wed 0500 EDT)

Consensus Forecast, HICP - Y/Y: 3.1%

Consensus Range, HICP - Y/Y: 2.6% to 3.2%

Consensus Forecast, Narrow Core - Y/Y: 2.6%

Consensus Range, Narrow Core - Y/Y: 2.5% to 2.6%

Pretty flat inflation readings expected for June versus May

at elevated levels the ECB has been unwilling to tolerate. The HICP is seen at

3.1 percent on year in June versus 3.2 percent in May. Core expected at 2.6

percent, the same as in May.

US ADP Employment Report for June (Wed 0815 EDT; Wed

1215 GMT)

Consensus Forecast, Private Payrolls - M/M: 118K

Consensus Range, Private Payrolls - M/M: to 85K to

130K

The consensus looks for payrolls up 118K in June versus 122K

in May, which would support the Fed's contention that the job market is

expanding in a stable way.

US Jobless Claims for Week 06/27 (Wed 0830 EDT; Wed 1230

GMT)

Consensus Forecast, Initial Claims - Level: 220K

Consensus Range, Initial Claims - Level: 210K to 225K

Claims appear stuck in this range of forecasts of 210K to

225K with the consensus looking for 220K this week versus 215K last week.

US PMI Manufacturing Final for June (Wed 0945 EDT; Wed

1345 GMT)

Consensus Forecast, Index: 55.7

Consensus Range, Index: 53.8 to 55.7

The consensus looks for no revision in the June final from

the June flash at 55.7, but up from 55.1 in May.

US ISM Manufacturing Index for June (Wed 1000 EDT; Wed

1400 GMT)

Consensus Forecast, Index: 53.8

Consensus Range, Index: 53.0 to 54.2

Manufacturing index seen almost unchanged at 53.8 in June

versus 54.0 in May, a remarkably resilient showing given all the turmoil around

commodity prices and supply disruptions flowing the Mideast war on top of all

the uncertainty flowing from Trump's tariffs.

US Construction Spending for May (Wed 1000 EDT; Wed 1400

GMT)

Consensus Forecast, M/M: 0.2%

Consensus Range, M/M: -0.2% to 0.8%

A moderate 0.2 percent increase is the call for May after

rising 0.4 percent in April.

US Motor Vehicle Sales for June (Any Time)

Consensus Forecast, Total Vehicle Sales - Annual Rate: 16.0

M

Consensus Range, Total Vehicle Sales - Annual Rate: 15.9

M to 17.25 M

Another flat reading is expected with sales at an annual

16.0 million in June after 16.1 million in May.

Thursday

South Korea CPI for June (Thu 0800 KST; Wed 2300 GMT;

Wed 1900 EDT)

Consensus Forecast, M/M: 0.3%

Consensus Range, M/M: 0.2% to 0.3%

Consensus Forecast, Y/Y: 3.3%

Consensus Range, Y/Y: 3.2% to 3.4%

CPI seen up 0.3 percent on month and 3.3 percent on year in

June after 0.5 percent and 3.1 percent in May. The year on year figure moving even

higher above 3 percent is bad news as rising prices for imported commodities

brings more inflation pressure. Markets increasingly expect the Bank of Korea

to respond by raising rates by 25 basis points in July to keep a lid on

inflation contagion.

Australia International Trade in Goods for May (Thu

1130 AEDT; Thu 0130 GMT; Wed 2130 EDT)

Consensus Forecast, Balance: A$2.175 B

Consensus Range, Balance: A$1.0 B to A$3.50 B

The surplus is seen wider at A$2.175 billion versus A$1.791

billion in April.

Eurozone Unemployment Rate for May (Thu 1100 CEST; Thu

0900 GMT; Thu 0500 EDT)

Consensus Forecast, Rate: 6.3%

Consensus Range, Rate: 6.3% to 6.3%

Another flat reading is the call with the jobless rate stuck

at 6.3 percent.

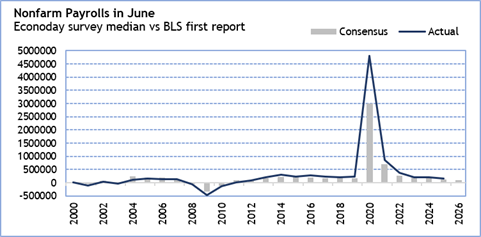

US Employment Situation for June (Thu 0830 EDT; Thu 1230

GMT)

Consensus Forecast, Nonfarm Payrolls - M/M: 114K

Consensus Range, Nonfarm Payrolls - M/M: 75K to 145K

Consensus Forecast, Unemployment Rate: 4.3%

Consensus Range, Unemployment Rate: 4.3% to 4.5%

Consensus Forecast, Private Payrolls - M/M: 124K

Consensus Range, Private Payrolls - M/M: 100K to 130K

Consensus Forecast, Manufacturing Payrolls - M/M: 4K

Consensus Range, Manufacturing Payrolls - M/M: 3K to

12K

Consensus Forecast, Average Hourly Earnings - M/M: 0.3%

Consensus Range, Average Hourly Earnings - M/M: 0.2%

to 0.3%

Consensus Forecast, Average Hourly Earnings - Y/Y: 3.5%

Consensus Range, Average Hourly Earnings - Y/Y: 3.4%

to 3.5%

Consensus Forecast, Average Workweek: 34.3

Consensus Range, Average Workweek: 34.2 to 34.3

A moderate 114K increase in payrolls is the call with the

jobless rate flat at 4.3%.

US Factory Orders for May (Thu 1000 EDT; Thu 1400

GMT)

Consensus Forecast, M/M: -2.1%

Consensus Range, M/M: -4.1% to 1.0%

After durable goods orders were reported down 4.5 percent

for May on a drop in aircraft orders, the call for factory orders is down 2.1

percent on the month.

Friday

China PMI Composite for June (Fri 0945 CST; Fri 0145

GMT; Fri 2145 EDT)

Consensus Forecast, Services Index: 53.5

Consensus Range, Services Index: 53.5 to 55.0

The consensus looks for another decent expansion in services

business activity with services expected at 53.5 in June versus 54.4 in May.

France Industrial Production for May (Fri 0845 CEST; Fri

0645 GMT; Fri 0245 EDT)

Consensus Forecast, M/M: -0.3%

Consensus Range, M/M: -0.4% to 0.5%

Industrial output expected to slip 0.3 percent in May from

April after edging up 0.1 percent in April.

France PMI Composite Final for June (Fri 0850 CEST; Fri

0650 GMT; Fri 0250 EDT)

Consensus Forecast, Composite Index: 47.6

Consensus Range, Composite Index: 47.6 to 47.6

Consensus Forecast, Services Index: 47.4

Consensus Range, Services Index: 47.4 to 47.4

The consensus looks for no revision in the final from the

flash at 47.6 for composite and 47.4 for services, suggesting ongoing

contraction.

Germany PMI Composite Final for June (Fri 0855 CEST; Fri

0655 GMT; Fri 0255 EDT)

Consensus Forecast, Composite Index: 48.0

Consensus Range, Composite Index: 48.0 to 48.8

Consensus Forecast, Services Index: 46.8

Consensus Range, Services Index: 46.8 to 48.1

The consensus looks for no revision in the final from the

flash at 48.0 for composite and 46.8 for services, suggesting ongoing

contraction.

Eurozone PMI Composite Final for June (Fri 1000 CEST;

Fri 0800 GMT; Fri 0400 EDT)

Consensus Forecast, Composite Index: 49.5

Consensus Range, Composite Index: 49.5 to 49.5

Consensus Forecast, Services Index: 48.9

Consensus Range, Services Index: 48.9 to 48.9

The consensus looks for no revision in the final from the

flash at 49.5 for composite and 48.9 for services.

UK PMI Composite Final for June (Fri 0930 BST; Fri

0830 GMT; Fri 0430 EDT)

Consensus Forecast, Composite Index: 49.4

Consensus Range, Composite Index: 48.7 to 49.4

Consensus Forecast, Services Index: 48.7

Consensus Range, Services Index: 48.7 to 53.1

The consensus looks for no revision in the final from the

flash at 49.4 for composite and 48.7 for services.

|